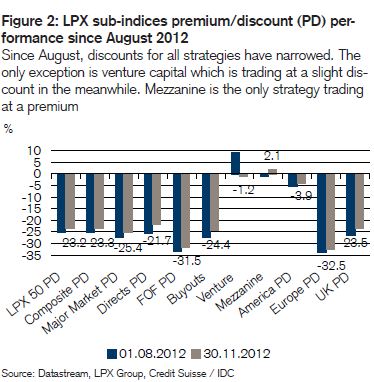

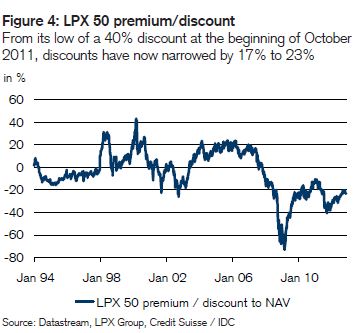

On a historical basis, the discounts are still wide. The 10-year average discount amounts to 8.4%, while the historical average discount since the inception of the index in January 1994 is a mere 4.3%. But discounts are also wide in comparison to private equity secondaries which are being sold at an average discount to NAV of 15%. Other sub-sectors within the listed fund sector (alternatives as well as equity funds) are trading at smaller discounts. This suggests that the wide discounts may be unjustified and have room to narrow further.

On a historical basis, the discounts are still wide. The 10-year average discount amounts to 8.4%, while the historical average discount since the inception of the index in January 1994 is a mere 4.3%. But discounts are also wide in comparison to private equity secondaries which are being sold at an average discount to NAV of 15%. Other sub-sectors within the listed fund sector (alternatives as well as equity funds) are trading at smaller discounts. This suggests that the wide discounts may be unjustified and have room to narrow further.

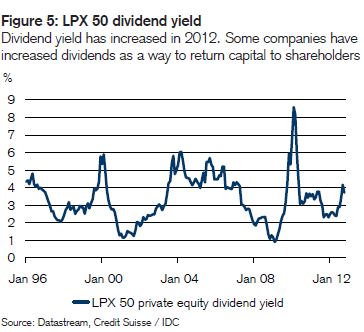

Managing discounts

The gap between share prices and net asset value (NAV) is a problem for investors. Discounts mean that investors cannot rely to receive the  “true“ value of their portfolio when selling their shares. This feature makes it unattractive to hold listed private equity in a portfolio. Criticism over the wide gap between NAV and share prices has led to increased activity on a manager’s side to take actions to reduce discounts. Capital

“true“ value of their portfolio when selling their shares. This feature makes it unattractive to hold listed private equity in a portfolio. Criticism over the wide gap between NAV and share prices has led to increased activity on a manager’s side to take actions to reduce discounts. Capital

is returned through dividends (see Figures 5) or share buyback programs. At its extreme, managers are pursuing realization strategies where portfolio companies are being sold over time, where it was not possible to get rid of stubborn discounts.

If portfolio companies can be sold at or above NAV (or even just above the discount the market prices in), the capital investors receive will exceed the share price. In most previous transactions, a sale price exceeding the NAV has been achieved. Assuming that this trend continues, this is another positive for the asset class’ future performance.

If portfolio companies can be sold at or above NAV (or even just above the discount the market prices in), the capital investors receive will exceed the share price. In most previous transactions, a sale price exceeding the NAV has been achieved. Assuming that this trend continues, this is another positive for the asset class’ future performance.

Mature portfolios but exiting investments is not so easy

Many private equity fund managers have mature portfolios, meaning that companies in their portfolios are ready to be sold. However, the exit environment is somewhat difficult at the moment. The main exit route is to sell portfolio companies to strategic (corporate) buyers. Besides that, going public through an IPO or selling a company in a secondary transaction to another private equity investor are common. Although

corporate buyers are rich in cash, the high level of uncertainty has caused M&A activities to stay low. The low appetite for M&A activity makes it difficult for private equity managers to sell their holdings. This may lead to lower exit prices or could cause managers to hold on to portfolio companies without being able to create additional value. Both would lead to lower returns.

Outlook – we see further upside

On the positive side, activities to manage discounts and return capital to investors should support the asset class. Stronger balance sheets  with better managed credit facilities, lower leverage levels and the reduction of over commitments are other positives. At present, we are tactically (1–6 months) as well as strategically (6–12+ months) positive on equities. LPE as a leveraged beta play on equities should continue to perform well in such an environment.

with better managed credit facilities, lower leverage levels and the reduction of over commitments are other positives. At present, we are tactically (1–6 months) as well as strategically (6–12+ months) positive on equities. LPE as a leveraged beta play on equities should continue to perform well in such an environment.

But there are also risks to consider. The sector depends on debt financing, and hence reluctance of banks to lend, new bank regulations or a future rate hike may negatively impact the asset class. However, central banks are indicating that their policy will remain supportive for longer. The exit environment characterized by low M&A appetite is another cloud on the horizon.

All in all, although discounts have narrowed considerably, we think the asset class has room to recover further from here. Despite the price upside potential in the near term, we would advise investors to take a longer-term stance as it may take time for value to be realized. Investors should be aware that LPE is a volatile asset class and risks may be considerable.

All in all, although discounts have narrowed considerably, we think the asset class has room to recover further from here. Despite the price upside potential in the near term, we would advise investors to take a longer-term stance as it may take time for value to be realized. Investors should be aware that LPE is a volatile asset class and risks may be considerable.

[email protected], +41 44 334 60 47